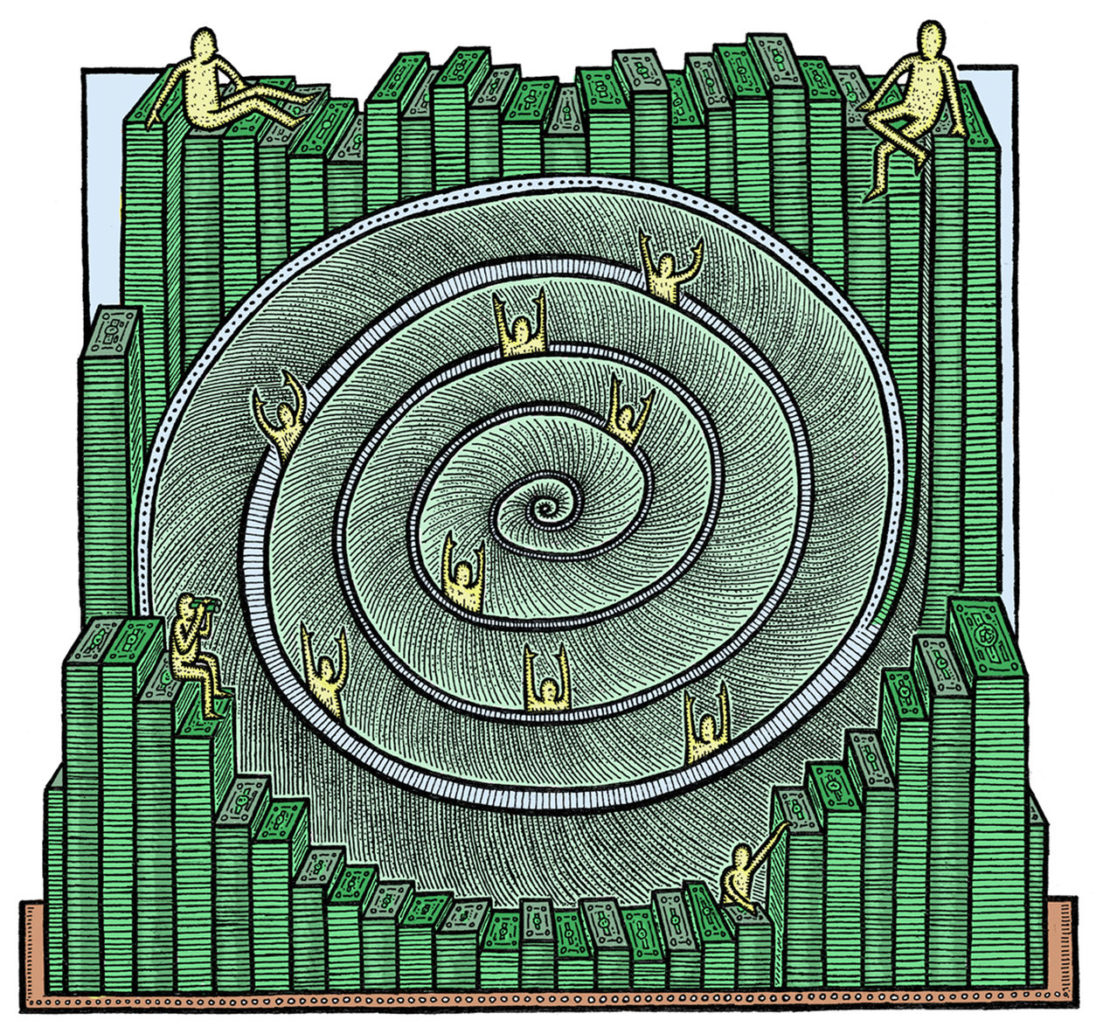

The Whirlpool Economy

Stagnation has spread like damp, deep into our economies. Japan is still struggling to resuscitate an inert economy 20 years after the implosion of a disastrous bubble initiated a prolonged slump. Much of Europe is in the grip of deflation. The German economy is running out of steam. The European Central Bank deems the situation so serious it is printing billions of euros to flood the markets with money. The US is doing better: the stock market, corporate profits and employment growth are all strong, at least for now. In 2014 the US economy added about 200,000 jobs a month. But the surge has been a long time coming: over the last five years growth has been less than two per cent. Few are completely confident this marks the start of a period of prolonged growth; it would take a remarkable US recovery to pull the world economy out of the doldrums the IMF has forecast for 2015. Even if the US economy grows, most people are unlikely to feel much better off: the vast majority of middle-income workers have not seen their wages rise for years. They live on narrow margins without savings to fall back on and are now unable to borrow from banks. Many people are hanging on to what they have, learning to get by rather than get ahead. Wages are stagnant even if, in some places, the economy is not.

Yet this state of stagnation is a very strange one, for it comes at time when our lives are in the midst of incessant change, much of it brought on by what claim to be radical innovations. Far from being stuck, modern life often seems highly fluid, provisional, uncertain and unpredictable. If the tech evangelists are to be believed, quite soon the skies of our cities will be buzzing with drones delivering packages, while down below computer-controlled electric cars will whisk us around as we catch up with crucial developments in our social media networks. Technologies such as 3D printing are about to come of age, offering not just fast ways to build homes and make furniture but custom designed prosthetics and even replacement organs. Every household could become a high-tech Downton Abbey with clever little robots unloading the dishwasher and laying out our neatly ironed clothes before we go to sleep in freshly made beds. Machines capable of rapid learning and recognising complex shifting patterns will be able to take over tricky jobs, like driving. Far from being stuck in a lifeless mire, we stand on the edge of an unruly and energetic cornucopia as these technologies combine, gather momentum and open up countless new opportunities for us to live better lives.

So which is it, a time of listless stagnation or disruptive innovation? The truth, of course, is that it is an odd mix of both.

In previous eras, from the middle ages through to the 1970s, stagnation went hand in hand with low innovation: the economy stagnated because there was little underlying dynamism, few new ideas and limited opportunities for entrepreneurship. Could we now live in an era where the economy is stagnating in partbecause there is so much innovation? Stagnation and innovation are combining to create a vicious whirlpool in which everything moves very fast and yet stays in the same place. Perhaps that helps to explain the dissonant feelings the always-on rush of modern life creates for so many people.

Technological tools that offer to make us more productive by undertaking tasks for us just end up helping us work longer hours, answering a torrent of emails, bleeps, updates and alerts. We feel busier than ever as digital diaries fill our days with meetings, yet oddly unproductive as achieving anything substantial requires extended periods of focus. One minute we’re over-stimulated by the screens that are our constant companions; the next we’re rendered powerless and listless by signal loss or the system going down.

All of these common feelings reflect a deeper disquiet: many feel richer and poorer at the same time. While wages stagnate, the squeezed middle classes hunt for bargains on moneysavingexpert.com; rent out their spare rooms on Airbnb; get driven around by someone earning a little extra by working for Uber on his day off; and entertain themselves for free on YouTube.

This would not be the first time our economies have suffered from a toxic mix thought impossible by orthodox economics. The 70s were a time of stagflation: slow growth combined with stubbornly high unemployment and high inflation. Now we live in a time of stagnovation: slow growth combined with incessant innovation and rising inequality. Are stagnation, innovation and inequality becoming locked together? Let’s take each ingredient of the cycle in turn.

Stagnation

Six years after the financial crash, despite extraordinarily low interest rates and central banks flooding the markets with easy money, economic growth in most of the developed world is as tepid and unreliable as a British summer.

We are not just suffering an exceptionally heavy hangover from the financial crash. It goes deeper than that, according to Larry Summers, former US treasury secretary and the most prominent exponent of the idea that our societies are in the grip of a ‘secular stagnation’. Summers argues the main problem is a deficiency of demand, public and private, which is keeping the economy well below potential. Others believe the problem is that the economy’s supply side potential has really contracted, owing in part to demographics. Either way, the argument is that the developed world economies are significantly smaller and slower growing than we imagined only a decade ago.

Most societies are ageing rapidly. As people prepare for longer lives so they will have to save more and consume less when they are younger. Outside China, governments do not have much appetite for or faith in stimulating higher growth through public spending, especially in Europe, where the OECD estimates that to meet the fiscal rules agreed in 2012, Italy and Portugal would have to run budget surpluses of 6 per cent to pay down debt. Whether, following the Syriza victory, Greece will stick to the rules, which demand a budget surplus of 9 per cent of GDP, remains to be seen. Paying down government debt will be a long haul, especially as slow wage growth drains government tax revenues. Nor will private borrowing and spending lift the economy rapidly as in the past. Consumers are paying off debts and finding it harder to borrow from banks, who have become latter-day converts to responsible lending.

Disinflation and deflation, such as the sharp fall in oil prices, helps to make people feel better off but only if these price falls are passed on to consumers. Even then, companies facing lower profits respond by cutting back on labour costs. What we gain as consumers, we stand to lose as wage-earners. Stagflation in the 70s created a vicious spiral of higher inflation, leading to higher wage demands, leading to higher inflation. Deflation is leading to lower prices, which is leading employers to reduce wage costs, which in turn makes people feel insecure and depresses demand.

The developed world economies are significantly smaller and slower growing than we imagined only a decade ago

Innovation

Even in the midst of stagnation, innovation seems to be quickening: back in 2004 the US granted 187,000 patents; in 2013 it was 300,000. Waves of new technologies will wash over the economy in the years to come, from Big Data and the Internet of Things, to medical treatments informed by genetics and nanoscale materials such as graphene. In the next decade we will start becoming familiar with a new species of intelligent machines that will mimic, augment, multiply and displace human brain-power much as electricity, steam and the combustion engine did human (and animal) muscle power in the 19th and 20th centuries. The most articulate exponents of this techno-optimism are Erik Brynjolfsson and Andrew McAfee, director and associate director respectively of the Center for Digital Business at the MIT’s Sloan School of Management. In their book, The Second Machine Age, they predict that we are about to reap the bounty of computers capable of understanding complex patterns, including language: so they drive cars, clean houses, stock shelves and analyse data. When machines this clever can be combined with human intelligence, connected through the web, we should all become vastly more productive and creative.

Explore

How secular stagnation came to Smurf village What we talk about when we talk about stagnationThe rub is that much of this innovation, in the context of stagnation and deflation, is aimed at eliminating jobs and lowering costs. Take one example; Google recently announced it had compiled a list of the locations of all businesses in France. One might think this would be a time-consuming task for a team of people. It took Google an hour. First, a staff member went through a few hundred images on Google’s Street View database, circling the street numbers and linking them to names of businesses. Google then fed that sample information to a machine-learning algorithm that would search similar examples in another 100m images on the database; and let the machines get on with it. Basic service jobs which involve information processing, analysis and administration will be turned over to far cheaper, increasingly intelligent machines in the next 10 years.

We are about to reap the bounty of computers capable of understanding complex patterns

Inequality

The transmission mechanism that turns rapid innovation into a sense of economic stagnation is inequality.

Innovation is making us immeasurably better off as consumers, providing myriad cheaper ways for us to get things done as we buy our entertainment, holidays, taxi services, hotel rooms and much more from vast online market places, or indeed get services for free. But innovation rewards people unequally as workers, entrepreneurs and investors.

Workers whose high skills are augmented by new technologies, like creative software programmers, are doing well: their skills are in high demand and short supply. At the bottom end, unskilled workers in call centres and data centres, supermarkets and warehouses, whose jobs are liable to be displaced by technology, are finding their wages flat or falling. The economy is creating jobs but many of them are low-productivity, low-pay service jobs. The result is that many young people find themselves doing work for which they are over-qualified: a quarter of all ‘entry level’ jobs in London are filled by someone with a degree, quite possibly one they have paid for themselves with debts they may never pay off. While job creation is strong, wage growth is subdued at best and the outlook is decidedly gloomy. Meanwhile, in many more markets a small group of winners – superstars, celebrities and entrepreneurs – seem to take the lion’s share of the profits, leaving almost everyone else to forage for slim pickings along the long tail of niche products and markets. The founders of Uber are billionaires; most Uber drivers work to augment the low and fluctuating incomes they earn doing another job. Apple sells hundreds of thousands of apps, most of them making little money for their designers, while the company that controls the entire ecosystem sits on a vast cash pile. When Ford Motor Company ruled the world it employed hundreds of thousands of people in manufacturing plants and offices all over the place. Facebook services hundreds of millions of consumers with just a few thousand staff in select city locations. The people best placed to profit from this innovative and entrepreneurial bonanza are already well off. When Alibaba, the Chinese shopping giant, had its Initial Public Offering in late 2014, the company was valued at $225bn. Most of the early investors were already rich and well-connected.

When the economy does grow, the largest share goes to people who tend to save more and spend less than those on lower incomes. There are only so many luxury yachts a billionaire can buy and only so many people are employed to make and maintain them. In a speech in October 2014, Janet Yellen, the chair of the US Federal Reserve, revealed that the poorest 50 per cent of Americans own just 1 per cent of the nation’s wealth, with an average net worth of just $11k, down from $22k in 1989. Meanwhile, despite low inflation and interest rates people on modest incomes will live on very narrow margins. Economist Robert Gordon forecasts that in the 25 years from 2007, US economic growth will average about 0.9 per cent a year – half the rate of the previous 25 years – but real disposable income for 99 per cent of the population will rise by just 0.2 per cent a year.

Innovation is not the only cause of this stark inequality; and inequality is not the only cause of stagnation. Many other factors are in play. Many mainstream economists, like Greg Mankiw at Harvard, argue the US economy is about to go into a long upswing which will make talk of stagnation irrelevant.

Yet it also seems increasingly likely that stagnation and innovation will be combined in a variety of ways. Long periods of glacial economic growth are likely to be punctuated by sudden, frenzied bubbles of investment in innovation. Some places associated with creativity and innovation, such as Williamsburg or Shoreditch, will boom; while areas nearby, like Brownsville and Tottenham, will languish. Organisations that serve consumers directly will be constantly innovating to attract attention, while those that supply them with basic commodities will find their markets stagnating: as supermarkets tempt us with ever more variety, so milk farmers complain they cannot make a living.

Stagnation and innovation will often come together as we try to combine the apparently impossible. We will feel as if we are richer (in free and low-cost technology), and yet poorer (in terms of disposable income) at the same time. The organisations we work for become increasingly fluid, flexible and provisional, while the social structure of our society becomes more stubbornly stuck. An ageing society in which people save more should lead to lower interest rates. But that will create more opportunities for fevered, speculative activity to build up around the latest brave new thing. Society will become more cautious and more reckless at the same time.

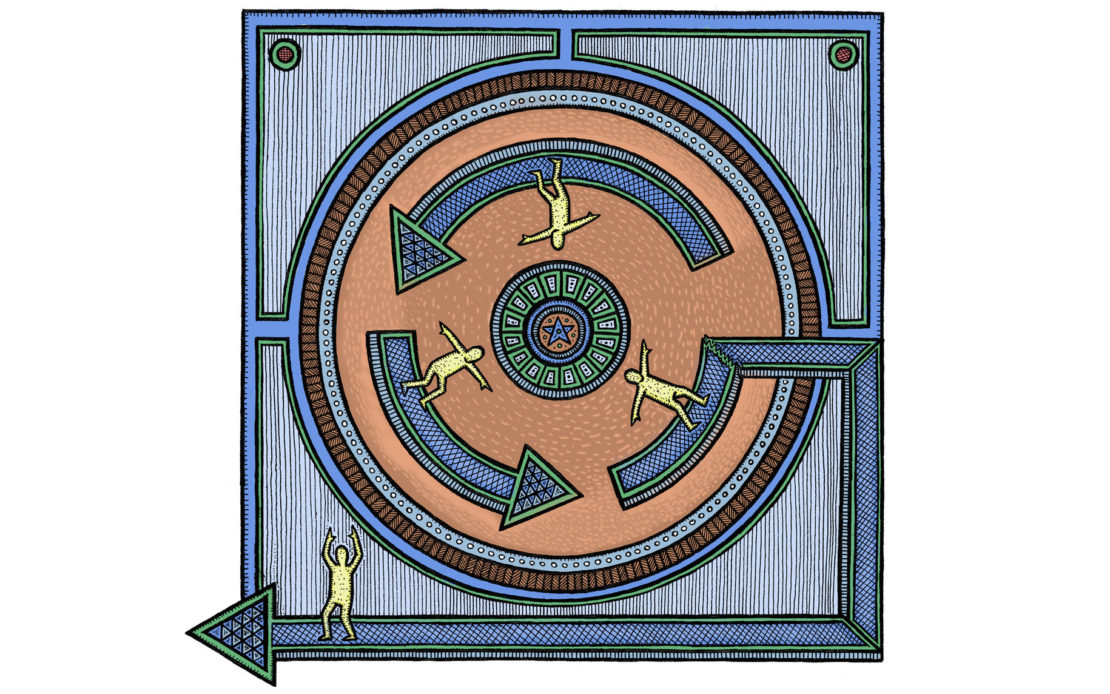

What hope is there that we might break out of this cycle? Here are just five ideas.

Focus on people on middle incomes

These are the people caught by the stagnovation cycle. They are working harder to see their disposable income barely rise. Increasing their security, incomes and spending power is the key to enabling them to escape from the whirlpool. Increasing their household incomes – many in this bracket are sharing their homes in multi-generational households or with strangers – will be a priority; in the short run through a decent living wage or, more radically, a negative income tax, or a universal basic income of the kind being debated in Switzerland. If inequality is key in translating innovation into stagnation, then a central aim of economic policy, including innovation policy, should be to reduce it by raising the incomes of those in the squeezed middle. That in turn means looking at the kind of basic innovations in the cost of housing, childcare, transport, energy and utilities which would make life more manageable for them. Allowing people on modest incomes to live well should become one of the chief goals of innovation policy.

What matters might not be economic growth

Growth measured in GDP – the exchange of physical goods and services – may be stagnant but that does not mean other aspects of our economic wellbeing are so flat. Ethnographic research on people living in London on limited incomes shows that they can live well when they are self-disciplined; not worried about keeping up with the Joneses; have strong relationships to rely on; and live in a safe area with decent public spaces. Consumers are innovating to make a little go a long way, for example by turning to the sharing economy to access what they need without owning it; and in renting out their idle assets to make a little extra. Learning how to live well without acquiring more stuff will be a key skill and measure of success. Many of the things we most value – friendship, recognition, trust, pride – cannot be bought on Amazon. GDP is becoming an increasingly misleading measure of economic wellbeing as so much of the intangible, digitally enabled economy of shared, user-generated content goes unrecorded: we are buying few CDs but that does not mean we are listening to less music than we used to. GDP growth may be stagnant in many economies but that does not mean our lives are, even as consumers.

Stop fighting the last economic war

Many of the economic policy assumptions of the past are now outdated. These days, interest rates look like remaining lower than we have been used to. The real interest rate at the peak of the business cycle in the US fell on average from 5 per cent in the 80s, to 2 per cent in the 90s and 1 per cent in the 2000s before dipping to 0.5 per cent since the Lehmann Brothers collapse. It is becoming harder to use low interest rates to stimulate the economy, especially in a time of low inflation. One controversial step would be to set a higher inflation rate – say 4 per cent – to stimulate the economy, put prices and wages on an upward trend and help reduce the burden of debt. If inflation were higher then real inflation-adjusted interest rates would be lower.

Alvin Hansen, the economist who raised the spectre of secular stagnation, did so in the late 30s just as the US economy was about to enter a sustained boom during and after World War II, brought on by government spending and new systems for mass education, production and consumption. Higher government spending to kickstart growth is not a panacea but it may become the only tool left to policy makers, especially in Europe, should a mixture of low interest rates and the European Central Bank’s money printing fail to reflate the stricken Eurozone.

Allowing people on modest incomes to live well should become a chief goal of innovation policy

Stop talking about disruptive innovation

Disruptive innovation has been the mantra of ambitious, high-tech startups since Clayton Christensen first popularised the idea in the late 90s in his book The Innovator’s Dilemma. He argued that disruptive radical innovators displaced complacent and shortsighted incumbents, and in the process opened up new markets and created larger industries. The trouble is that disruption can be quite unpleasant if you are on the receiving end and have few opportunities to find alternative employment with similar wages and benefits. The fact that a few entrepreneurs become billionaires in the process does little to soften the blow.

The innovative, high-tech sectors need a different story of socially useful innovation, which generates new jobs and augments existing ones; while addressing the spiralling costs of things like energy, health and social care that matter to median-income households.

Cities will spawn the best solutions

Factories, supermarkets and malls were among the key institutions in the boom era of industrial mass production and consumption. In our era, networks and clusters in cities will be the most important places where new solutions will emerge. Cities at their best have an unruly, irrepressible energy. They are where new lifestyles, technologies and forms of organisation for sharing, collaborative consumption and crowdfunding take root. New technologies and lifestyles spread fast in cities. Most new companies of note will be founded in cities rather than in suburban industrial and science parks.

Yet cities are where inequalities are also at their starkest and where solutions to address the needs of the middle classes are most urgently needed. A 2012 Pew Research Center study found that 27 of the 30 largest US metropolitan areas were becoming segregated into areas of exclusively low- or high-income households, with markedly fewer mixed- and middle-income neighbourhoods. A University of Toronto study found the same was true of most Canadian cities.

Cities that 20 years ago were caught in a spiral of decline are the resurgent engine rooms of the knowledge-intensive, globally interconnected service economy. Yet middle-income, middle-class workers feel increasingly left behind.

The most successful cities, socially and economically, will be those that create inclusive, fair models of growth. Cities like Seoul, where the local government sees raising incomes and providing public services more effectively as two sides of the same coin, with a programme to promote the social and sharing economy, especially to middle-aged, middle-income workers who have been made redundant from large companies. In Curitiba in Brazil, the city government has invested heavily in localised economic development initiatives, coupled with novel forms of housing development based on mass self-building, community-based public service solutions and low-cost public transport based on high-speed bus lanes.

In the 90s, creative cities that managed to remake themselves attracted all the attention. In future that will not be enough. City leaders will need to find ways to grow fairly, inclusively. The cities that manage to do that will show us a way out of the whirlpool.